Take advantage of every homebuying benefit you’ve earned! Download the Made 4 More app for accurate listings, zero spam, and no hidden fees—so you can confidently explore the best homes and make the most of your VA loan opportunity.

For a lot of Veterans, homeownership feels like climbing a mountain with a backpack full of bricks. Rising prices, higher interest rates, and down payment myths have convinced many people that buying a home is out of reach. But here’s the truth: many Veterans are sitting on one of the most powerful homebuying benefits available — and they don’t even realize how much it can do for them.

The VA home loan benefit has helped millions of Veterans become homeowners for more than 80 years. Yet surprisingly, many eligible buyers still misunderstand how it works. And those misunderstandings could be costing them thousands of dollars — or worse, delaying their dream of owning a home.

Let’s break down some of the biggest myths about VA loans and why this benefit could be your ticket to homeownership sooner than you think.

The Biggest VA Loan Myth? “I Need a Huge Down Payment”

This is the misconception that stops a lot of Veterans before they even start.

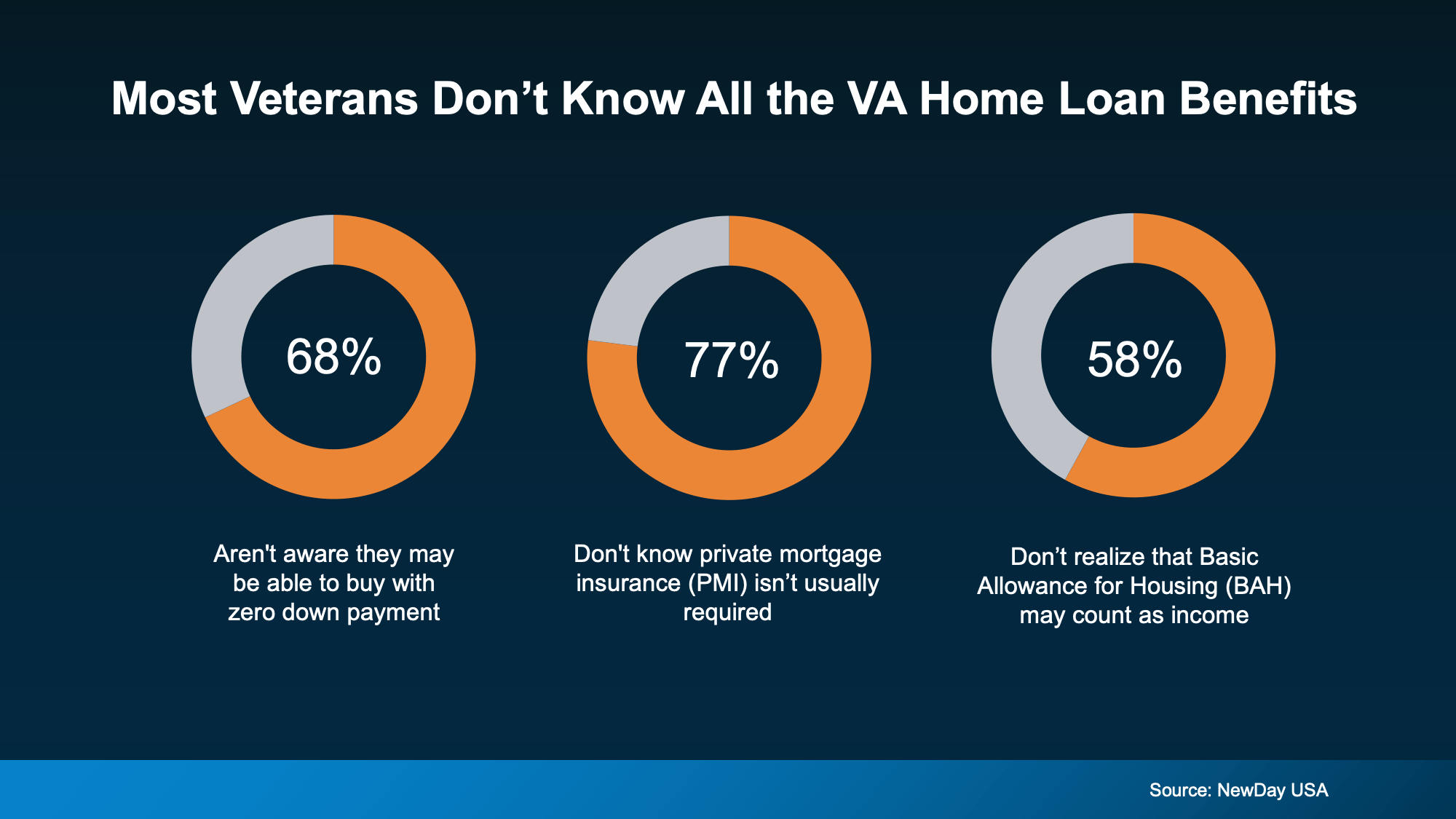

Many buyers assume they need to save $10,000, $20,000, or even more just to buy a home. That’s enough to make anyone feel discouraged. But with a VA loan, qualified buyers may be able to purchase a home with zero money down.

Yep — zero.

That means instead of spending years trying to build up a massive savings account, you could focus on finding the right home now. It’s like getting a fast pass at an amusement park while everyone else is standing in line waiting.

And in today’s market, time matters.

Closing Costs Might Be Lower Than You Think

Here’s another surprise many Veterans don’t know: VA loans can limit certain closing costs buyers have to pay.

Translation? More money stays in your pocket.

When buyers hear the phrase “closing costs,” they often picture another financial mountain to climb. But VA loan protections can help reduce some of those upfront expenses, making homeownership feel a lot more manageable.

Pair that with little-to-no down payment, and suddenly buying a home doesn’t seem impossible anymore.

No PMI Could Save You Thousands

Let’s talk about one of the sneakiest costs in homeownership: PMI.

Private Mortgage Insurance (PMI) is typically required on conventional loans when buyers put down less than 20%. That monthly fee can quietly drain your wallet month after month.

The good news? VA loans typically don’t require PMI.

That’s huge.

Depending on the loan amount, buyers using conventional financing could spend hundreds of dollars every month on PMI alone. Over time, that adds up to thousands of dollars that could’ve gone toward vacations, savings, investments, or simply enjoying life.

With a VA loan, that money may stay where it belongs — in your bank account.

Your Military Housing Allowances Could Help You Qualify for More

If you’re active duty or a qualifying reservist, this part is especially important.

Your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward your qualifying income for a VA loan.

A lot of buyers run the numbers without including these benefits, which can lead them to believe they qualify for less than they actually do.

Think of it like forgetting to count part of your paycheck. That missing piece could make a major difference in your buying power.

And because BAH and BAS are non-taxable, they can strengthen your loan qualification even more.

Why So Many Veterans Wait Too Long To Buy

Honestly, most Veterans aren’t held back by lack of opportunity — they’re held back by lack of information.

They assume:

- Buying requires a huge down payment

- Monthly payments will be too high

- They won’t qualify

- The process is complicated

But the reality is, VA loans were specifically designed to make homeownership more accessible for those who served.

The key is working with the right professionals who actually understand how to maximize the benefit.

Homeownership May Be Closer Than You Think

If you’ve served our country, you deserve to know all your options.

Whether you’re active duty, a Veteran, or a reservist, your VA loan benefit could help you:

- Buy sooner

- Save thousands upfront

- Lower your monthly costs

- Build long-term wealth through homeownership

And in a market where every dollar counts, those advantages can be game-changing.

Bottom Line

Too many Veterans assume homeownership is out of reach when they may already have one of the best financing tools available. VA loans can open doors faster, reduce upfront costs, and help buyers keep more money in their pockets.

The biggest mistake? Not exploring the benefit at all.

📲 Call or text us today at 855-935-MORE to learn how your VA loan benefit could help you buy a home sooner than you thought.

Check out this article next