Don’t let scary headlines or bad data steer you wrong. Download the Made 4 More app for the most accurate listings—without your info being sold—so you can make confident moves in today’s market.

You’ve seen it.

“Foreclosures are rising.”

And if you lived through 2008, your brain probably went straight back there. Empty streets. Bank-owned homes. Panic. Chaos.

But here’s the truth no headline is telling you:

This is not 2008. Not even close.

And if you’re a real estate agent, understanding this difference isn’t just helpful — it’s a massive opportunity to educate, lead, and win trust right now.

Let’s break it down.

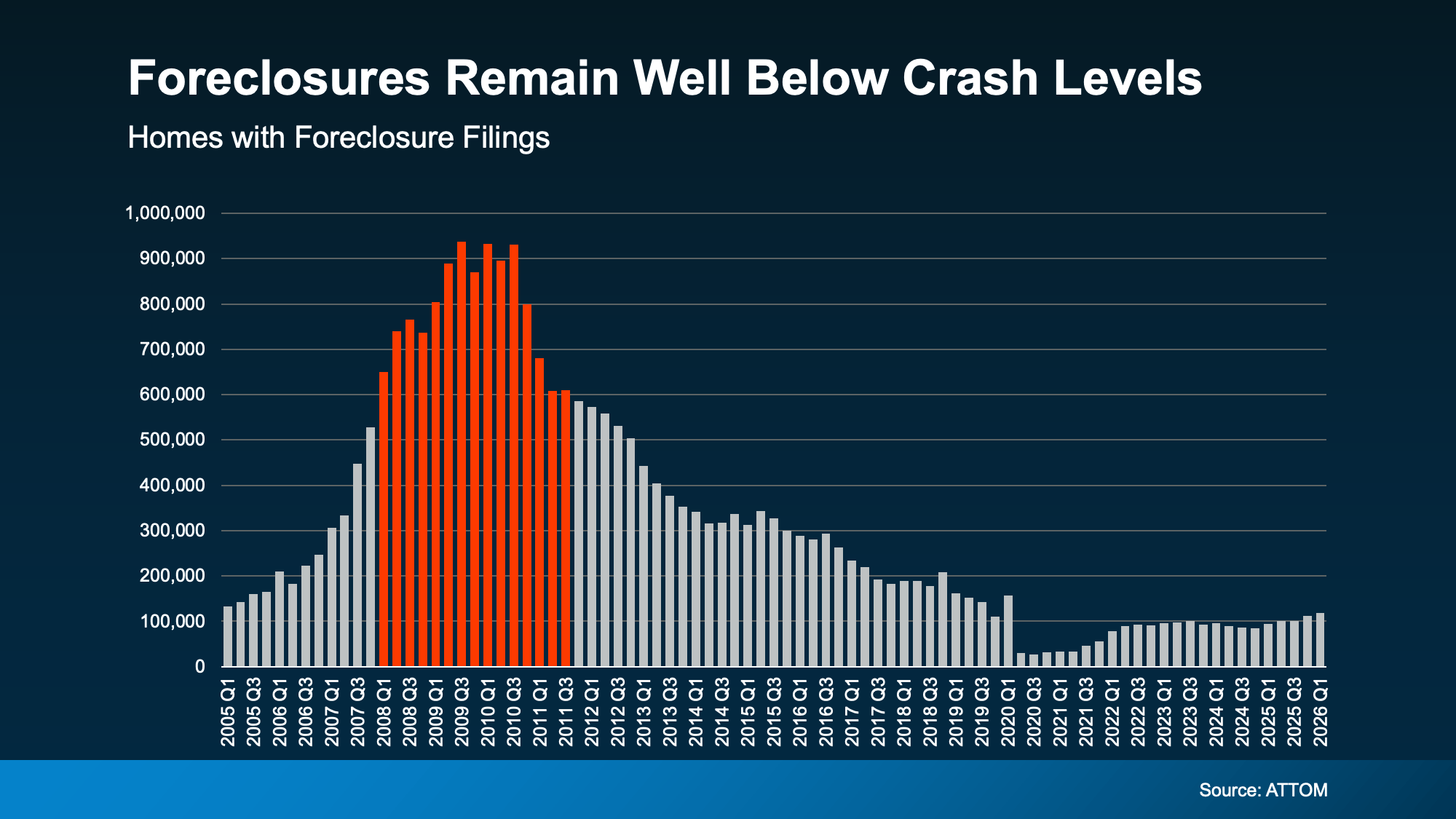

📉 Foreclosures Are Up… From Unnaturally Low Numbers

Yes — foreclosure filings are up 26% year over year, according to ATTOM.

Yes — they’ve been rising for five straight quarters.

But here’s what most people are missing:

2020 and 2021 were not normal years.

The government literally paused foreclosures during the pandemic. Those numbers you saw then? They were artificially suppressed. Frozen. Unreal.

So when you compare today’s numbers to those years, it looks like a spike.

But when you compare today to 2017, 2018, 2019 — the last “normal” market?

We’re still below those levels.

This isn’t a crash.

This is the market returning to its baseline.

💰 The $295,000 Reason This Isn’t Another Housing Collapse

Here’s the game-changer.

According to Cotality, the average homeowner today is sitting on about $295,000 in equity.

Read that again.

In 2008, people owed more than their homes were worth. They were trapped. Selling wasn’t an option. Foreclosure was the only exit.

Today?

If someone gets behind on payments, they can sell, pay off their debt, protect their credit, and often walk away with money.

That one difference changes everything.

And it’s the main reason foreclosures today are unlikely to spiral out of control.

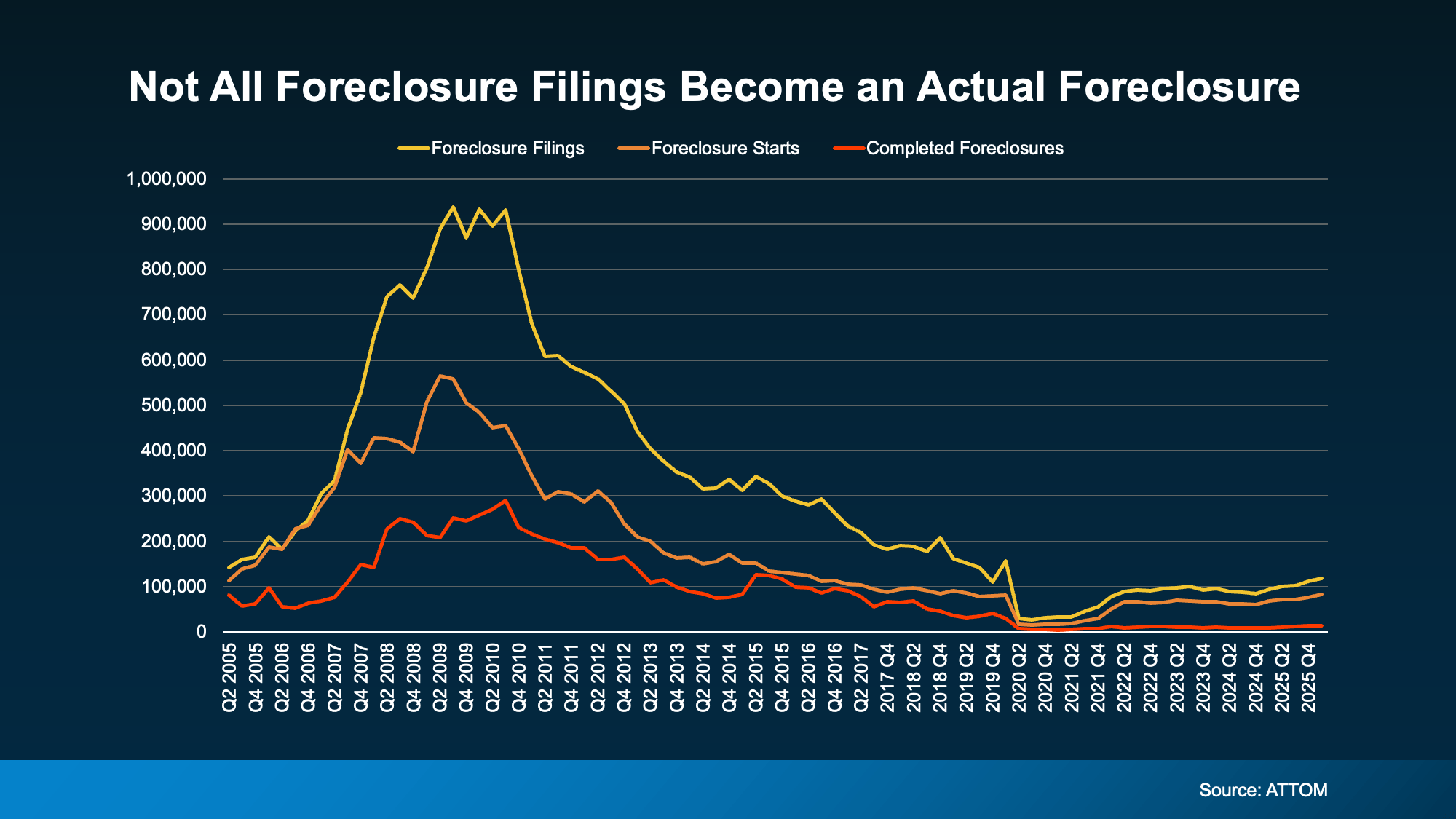

📊 Most “Foreclosure Filings” Never Become Foreclosures

This is the part no one is talking about.

ATTOM tracks three things:

- Foreclosure filings

- Foreclosure starts

- Completed foreclosures (where someone actually loses their home)

That last number? The one that matters?

It’s way lower.

Because homeowners are finding solutions before it gets there — selling, refinancing, negotiating, or using their equity as leverage.

Which means what we’re seeing now is early-stage distress, not housing collapse.

🤝 Banks Don’t Want Homes — They Want Solutions

Here’s another misunderstood truth.

Banks hate foreclosures. They’re expensive. Slow. Complicated.

They would much rather:

- Offer repayment plans

- Pause payments (forbearance)

- Modify the loan

- Or let the homeowner sell

The earlier someone asks for help, the more options they have.

And this is where educated agents become invaluable guides in their communities.

🎯 Why This Is a Huge Opportunity for Agents Right Now

This market is creating a new type of seller:

- People who are nervous

- People who are behind

- People who think they’re out of options

- People who are scared of “another 2008”

And they are desperate for someone who understands the real data.

Not fear.

Not headlines.

Facts.

Agents who can calmly explain this are becoming the most trusted voices in their markets.

This is not a foreclosure wave.

This is a massive education moment.

And education builds listings.

🧠 The Bottom Line

Yes, foreclosures are rising.

But they’re still historically low.

And thanks to record equity, today’s homeowners have exits that didn’t exist in 2008.

The market isn’t collapsing.

It’s normalizing.

And agents who understand this will lead the conversation while everyone else repeats scary headlines.

Call or text us at 855-935-MORE to learn how we help agents turn market confusion into listing opportunities.

Check out this article next