📲 Don’t let confusing rates or hidden costs keep you from your perfect home! Download the Made 4 More app for the most accurate listings—your info stays private. Find the best deals and make confident moves—start today!

Mortgage rates have been playing a tricky game this year. They dipped into the upper 5% range a couple of times—but just as quickly, they bounced back into the low 6s. If you saw that and thought, “Ah, I missed it!”, you’re definitely not alone.

But here’s the reality: the “magic” of the 5s isn’t as magical as it feels.

The Payment Difference Isn’t As Dramatic As You Think

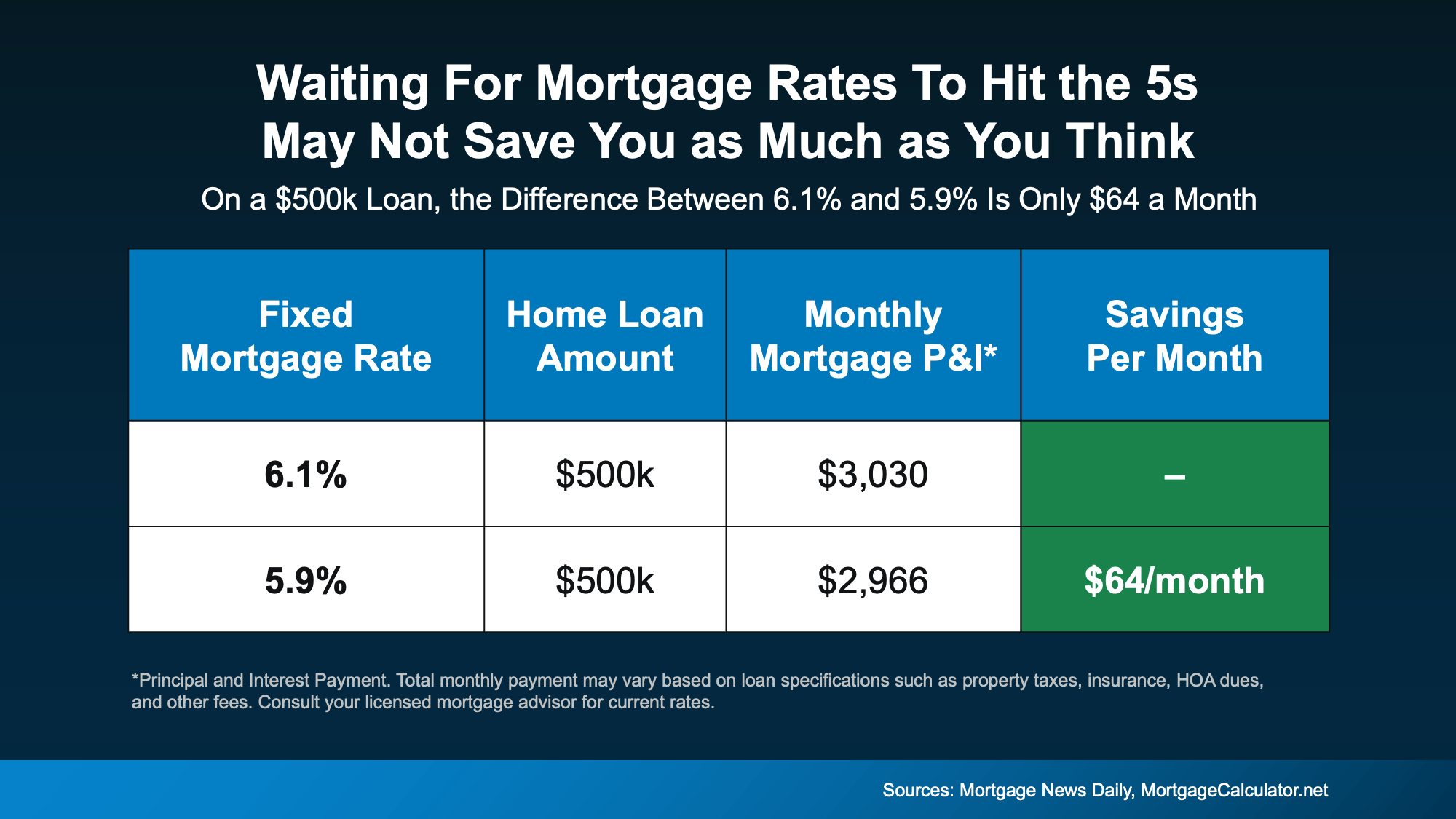

Let’s do a quick reality check. Say you’re looking at a $500,000 home loan:

- At 6.1%, your principal and interest payment is roughly $3,030/month

- At 5.9%, it drops to about $2,966/month

That’s a difference of only $64 per month. Not $300. Not $500. Sixty bucks.

Sure, over time it adds up—but it’s far from the life-changing swing many buyers imagine when they say they’re “waiting for the 5s.” The mental impact of seeing a 5 in front of your rate can feel huge—but financially? You might barely notice.

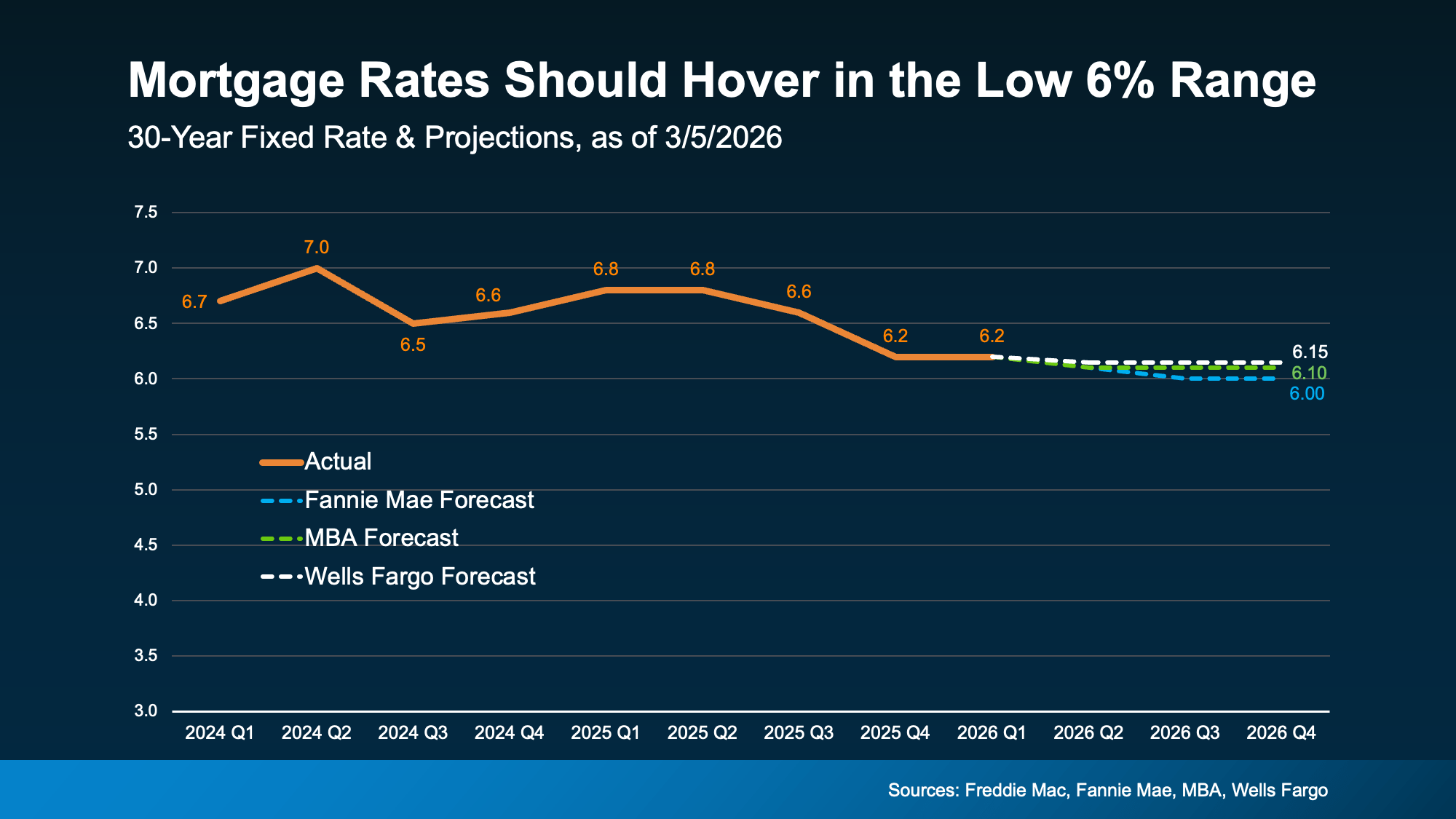

Experts Say Don’t Expect a Major Drop

Most housing economists aren’t forecasting a return to 5% territory anytime soon. Rates may bounce around the high 5s here and there, but the expectation for the year? Low 6s.

Waiting for a deep drop may not pay off the way you’re hoping. The truth is, chasing the “perfect” rate could mean missing out on the homes that are actually within your reach right now.

Ask the Bigger Question: Can You Afford Today’s Payment?

Instead of worrying about missing the 5s, ask yourself:

“Does today’s monthly payment work for my budget?”

If it fits, and you’ve found a home that ticks your boxes, the difference between 6.1% and 5.9% isn’t the dealbreaker. It’s just a small piece of the bigger home-buying puzzle.

And remember—mortgage rates aren’t permanent. If they drop later, you can always refinance. But you can’t refinance a home you never bought.

Waiting Feels Safe, But It Might Not Be Strategic

It’s natural to want the “best” rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will actually change their monthly payment.

Consider this: a year ago, rates were in the 7s. Now they’re hovering in the low 6s—a big shift for many buyers. If you paused your plans when rates were higher, now is a perfect time to re-run the numbers. The payment might be more manageable than you think.

Bottom Line: Don’t Wait for the Magic Number

Sitting on the sidelines waiting for rates to drop further may not give you the payoff you expect. Instead, focus on what you can afford now and homes that meet your needs.

Let’s double-check your numbers together—you might find your dream home is already within reach.

📞 Call or text us today at 855-935-MORE to see what your payment could be!

Check out this article next