Don’t let scary headlines or bad data keep you from making smart real estate decisions! Download the Made 4 More app for the most accurate listings and real-time market insights—without your info being sold. Find the best opportunities with confidence and stay ahead of today’s housing market. Get started today!

Turn on the news lately and you’ll probably hear the same scary phrase repeated over and over: America’s mortgage debt just hit a record high.

Cue the dramatic music. 😱

And sure, at first glance, that sounds alarming. A lot of people instantly think back to 2008 and wonder if history is about to repeat itself. But here’s the problem with most headlines: they only tell part of the story.

It’s like looking at the gas gauge in your car without realizing the tank got twice as big.

Yes, mortgage debt is high. But homeowner wealth? Even higher. And that changes the entire conversation.

The Mortgage Debt Number Is Real — But It’s Missing a Massive Piece of the Puzzle

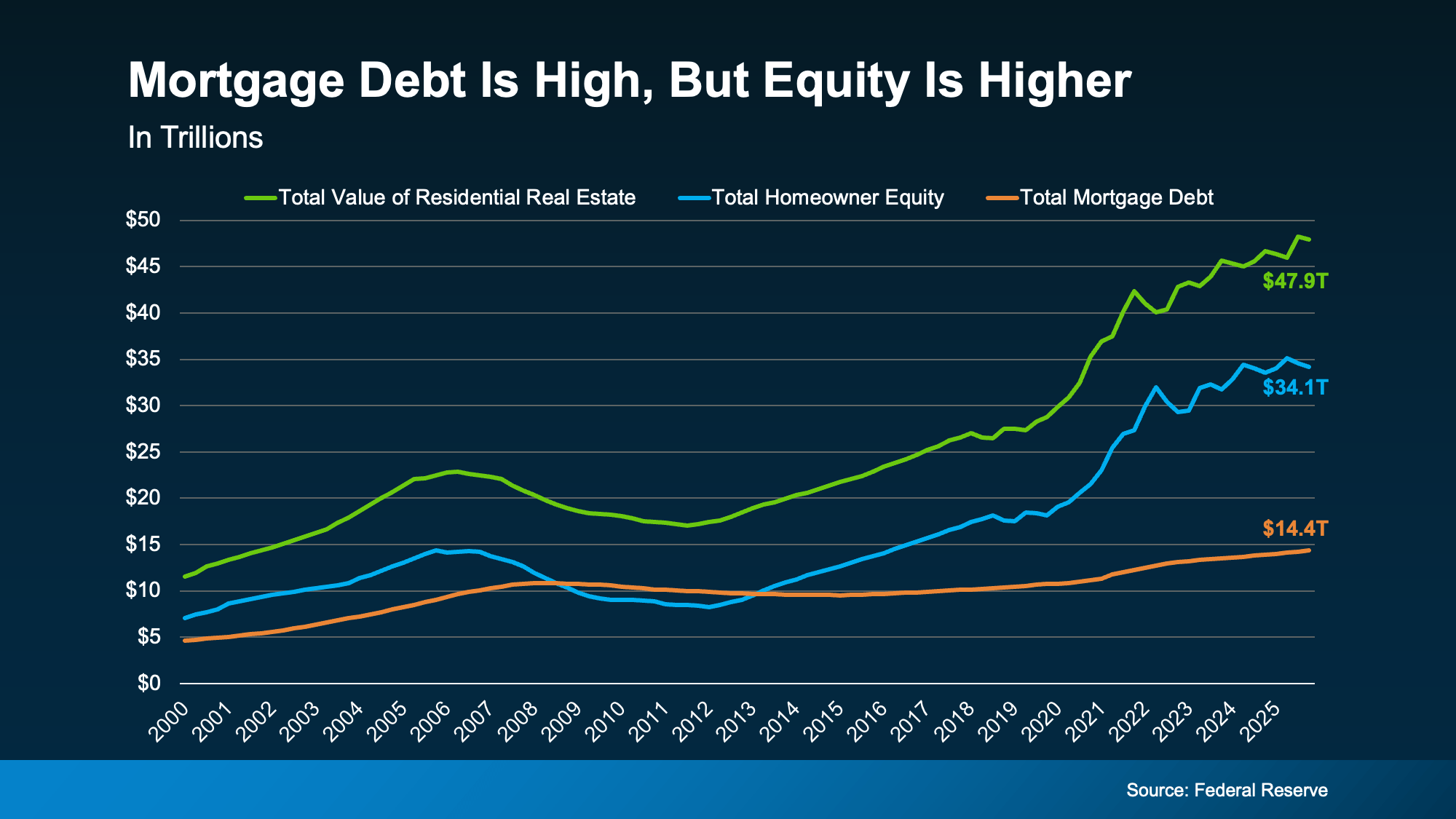

According to the Federal Reserve, mortgage debt in the U.S. is sitting around $14 trillion. That’s the highest level ever recorded.

Sounds terrifying, right?

Not so fast.

What those headlines often skip is this: home values and homeowner equity have exploded too.

Right now, the total value of homes across the country is nearly $48 trillion, while homeowner equity is sitting around $34 trillion. That means Americans collectively own far more of their homes than they owe.

That’s a huge distinction.

During the 2008 housing crash, many homeowners were upside down. They owed more on their mortgage than their home was worth. That’s what created panic, foreclosures, and financial chaos.

Today? It’s the complete opposite.

Most homeowners are sitting on a mountain of equity like a financial safety net under a tightrope. Even if the market cools, many owners still have substantial cushion protecting them.

That’s not a fragile market. That’s a fundamentally different market.

Today’s Homeowners Are in a Much Stronger Position

Here’s where things get even more interesting.

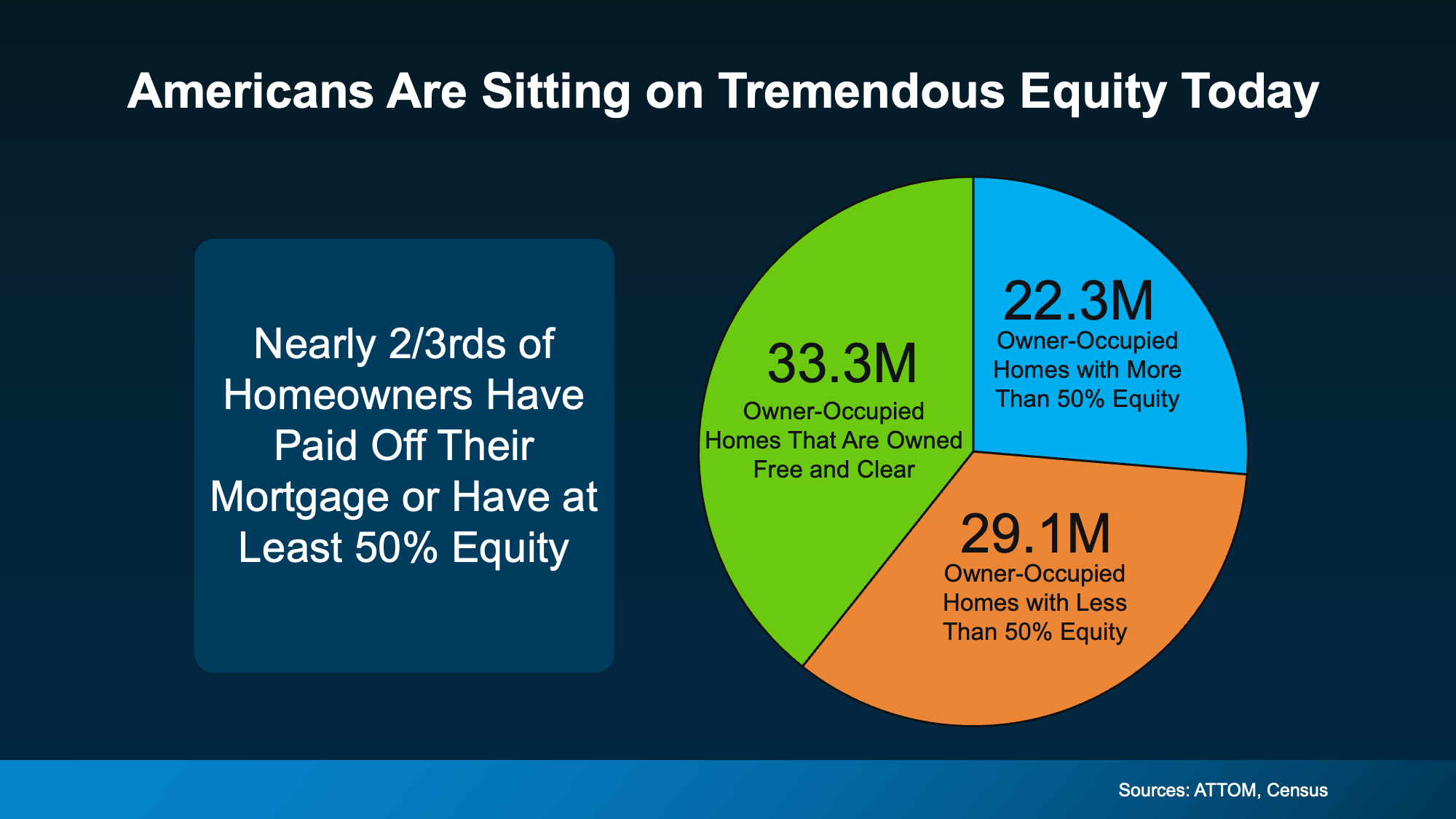

Millions of Americans don’t even have a mortgage anymore.

Roughly 33 million homes in the U.S. are owned free and clear. No monthly mortgage payment. No lender attached. Just outright ownership.

On top of that, another huge group of homeowners has already built more than 50% equity in their homes.

When you combine those groups together, nearly two-thirds of homeowners are sitting in extremely stable financial positions.

That’s not exactly the recipe for a housing collapse.

Of course, there are still homeowners with lower equity positions, especially recent buyers. But building equity takes time, and many of those homeowners are still financially healthy and making payments consistently.

The reality is today’s housing market isn’t balancing on a house of cards. It’s standing on a much stronger foundation than many people realize.

Why This Matters for Buyers and Sellers Right Now

If you’re a buyer, this is important because it helps cut through the fear-driven headlines.

The market may feel uncertain at times, but uncertainty doesn’t automatically equal disaster. In fact, many homeowners are financially stronger today than ever before.

And if you’re a seller? This equity story could be a game changer for you.

Many homeowners are sitting on enough equity to:

- Move up into a larger home

- Downsize comfortably

- Invest in another property

- Pay off debt

- Or simply walk away with significant cash at closing

That’s why so many people are re-entering the conversation about buying or selling, even with today’s mortgage rates.

The Market Isn’t Perfect — But It’s Not 2008 Either

Let’s be real. Every housing market has challenges.

Affordability is still tough. Mortgage rates remain higher than many buyers want. Inventory is still tight in many areas.

But comparing today’s market to 2008 is like comparing a summer thunderstorm to a category-five hurricane.

Back then, homeowners had little equity, risky lending was everywhere, and the system was overloaded with bad debt.

Today, lending standards are far stricter, homeowners have record levels of equity, and the majority of borrowers are locked into historically low fixed mortgage rates.

Those differences matter. A lot.

What Smart Agents Understand About This Market

Here’s the truth many people miss: markets like this create opportunity for agents who know how to educate instead of just sell.

Consumers are overwhelmed with conflicting headlines. They don’t just need salespeople. They need trusted advisors who can explain what’s really happening in plain English.

That’s where strong agents separate themselves from the crowd.

At Made 4 More Realty, we believe real estate is about helping people make smart, confident decisions — not pushing fear or hype.

And in a market full of noise, that approach matters more than ever.

Bottom Line

Yes, mortgage debt is at a record high.

But so is homeowner equity.

That’s the part the headlines conveniently leave out.

The housing market today is built on a much stronger financial foundation than it was during the last crash, and most homeowners are in remarkably stable positions.

If you’ve been trying to make sense of the market, wondering whether it’s the right time to buy, sell, invest, or even start a career in real estate, we’re here to help.

Call or text us today at 855-935-MORE and let’s talk strategy. No pressure. Just real answers.

Check out this article next