📱 Don’t let bad data or hidden fees cost you your dream home! Download the Made 4 More app for the most accurate listings—without your info being sold. Find the best deals with confidence. Get started today!

You’ve probably seen the headlines.

“Foreclosures are increasing.”

“Market trouble ahead?”

And if you’ve been around the real estate world long enough, your brain may jump straight back to 2008. Totally understandable. That crash left a mark.

But here’s the truth most headlines skip: today’s housing market is nothing like the one that triggered the crash.

In fact, one key data point shows we’re nowhere near a foreclosure wave. Let’s break it down.

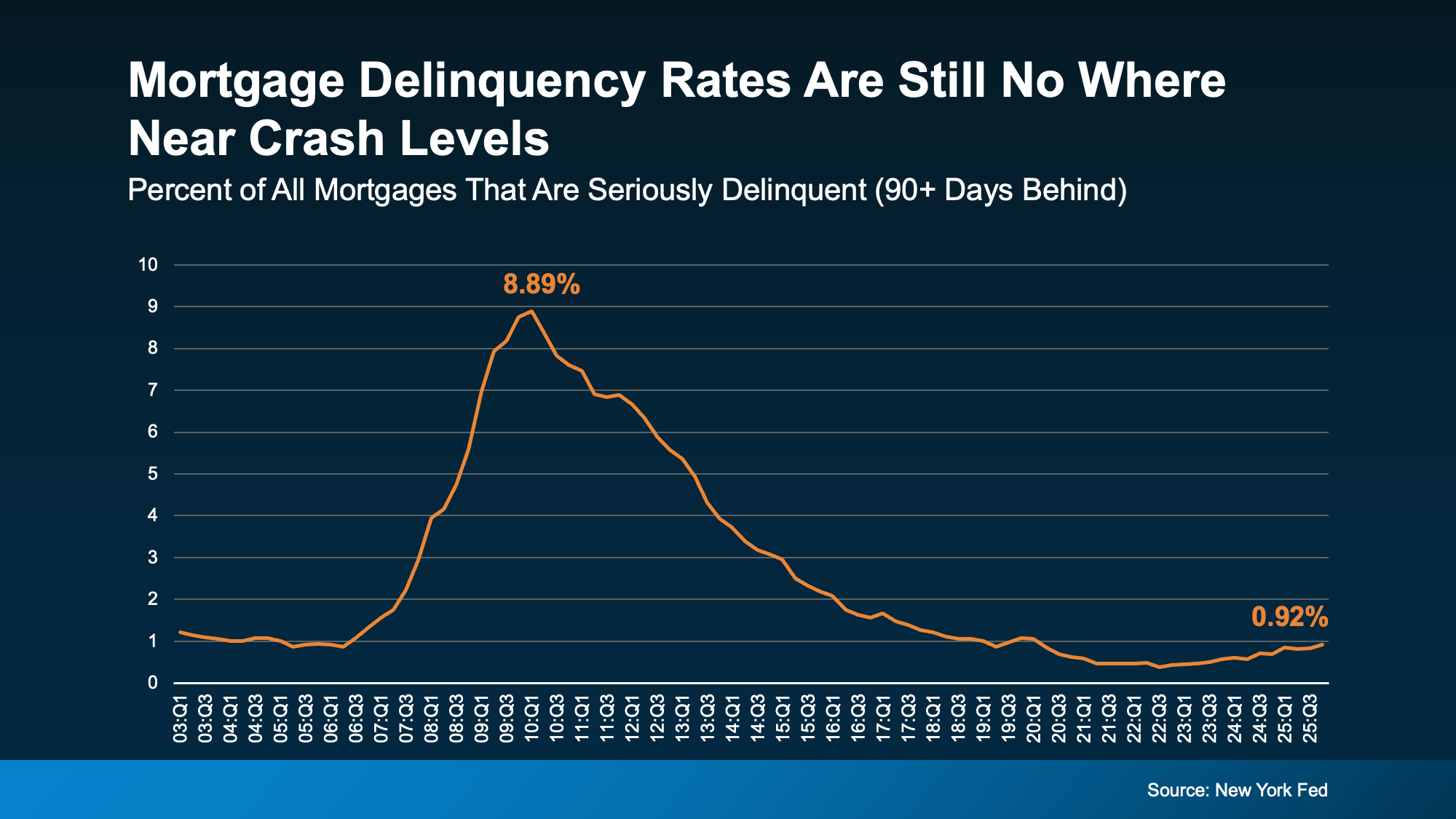

📉 Serious Mortgage Delinquencies Are Still Very Low

First, let’s talk about serious delinquencies—that’s when a homeowner is 90+ days behind on their mortgage payments.

Yes, they’ve ticked up slightly.

But zoom out for a second.

Right now, about 1% of mortgages are seriously delinquent. That’s 1 out of every 100 homeowners.

Compare that to the housing crash years when serious delinquencies reached around 9%, or 1 in every 11 homeowners.

That’s not a small difference.

That’s the difference between a ripple and a tidal wave.

Even more important? Not every delinquency becomes a foreclosure.

Many homeowners work out payment plans with lenders. Banks actually prefer this outcome because foreclosures are costly and time-consuming.

So even though delinquencies exist, foreclosure filings remain extremely low.

🏠 Actual Foreclosure Numbers Are Tiny

Let’s put the real foreclosure numbers into perspective.

Right now, only about 0.3% of homes in the U.S. are in the foreclosure process.

That’s 3 out of every 1,000 homes.

Not exactly a housing apocalypse.

In reality, the current market is experiencing something closer to normalization, not a collapse. During the pandemic years, foreclosure activity dropped to record lows, so today’s slight increase is simply the market returning to typical levels.

Think of it like a thermostat adjusting—not a fire alarm going off.

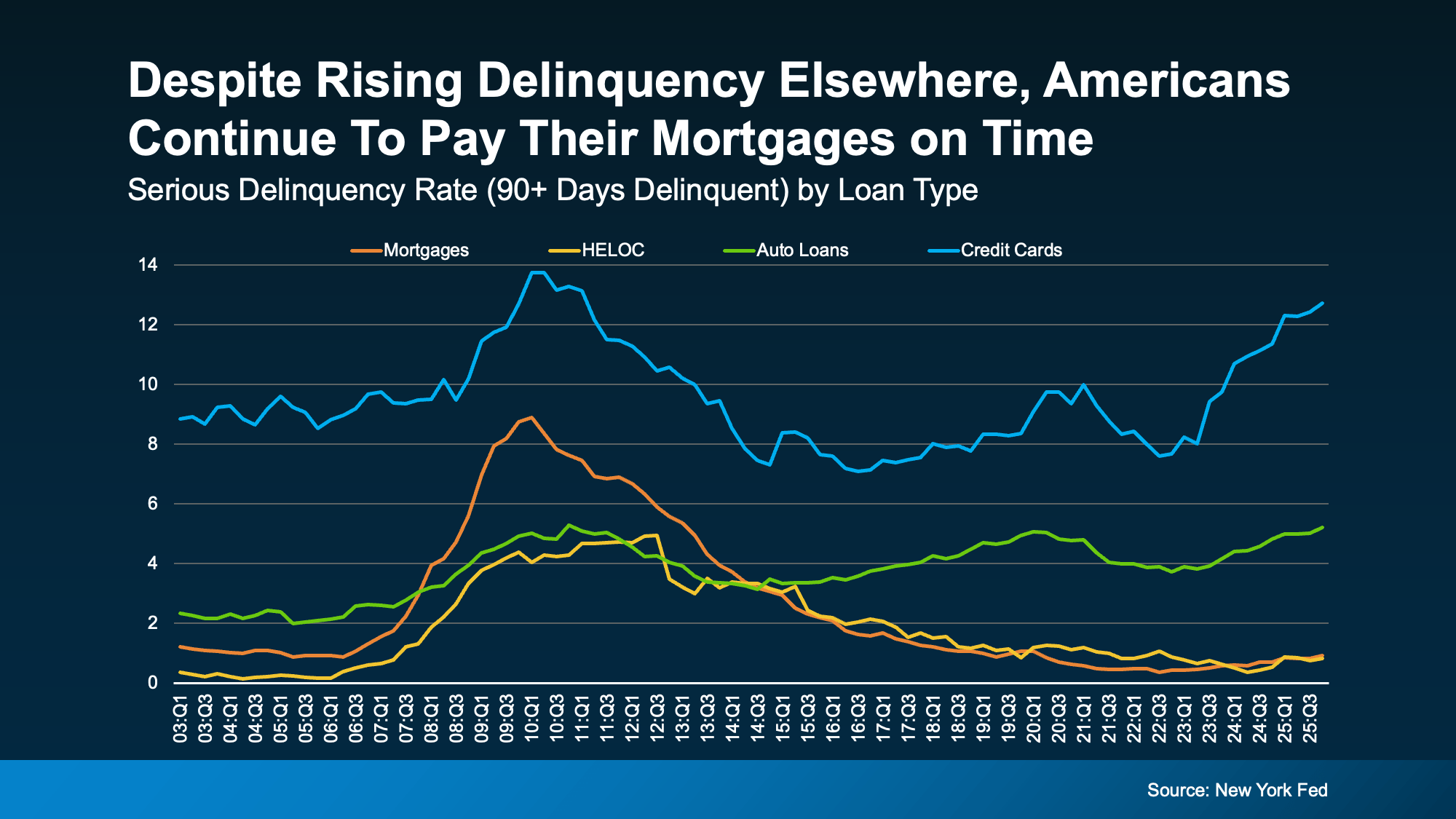

💳 People May Fall Behind on Debt… But They Protect Their Homes

Here’s something fascinating about consumer behavior.

When households feel financial pressure, they prioritize their mortgage payment above almost everything else.

Credit cards?

Auto loans?

Personal loans?

Those are usually the first to fall behind.

But the mortgage? That’s different. Because no one wants to lose their home.

Recent data shows delinquencies have increased far more in credit cards and auto loans than in mortgages. Homeowners are doing everything they can to stay current on housing payments.

That’s a powerful signal about the strength of today’s housing market.

💰 Home Equity Is the Game Changer

The biggest difference between today and the 2008 crash?

Home equity.

Over the past several years, homeowners have built massive equity gains thanks to rising home values.

And equity creates options.

If a homeowner runs into financial trouble, they often don’t need to go into foreclosure. Instead, they can simply sell the home, pay off the loan, and walk away with money in their pocket.

That wasn’t the case in 2008.

Back then, millions of homeowners owed more than their homes were worth. Selling wasn’t an escape route—it was a dead end.

Today?

It’s often the smartest move available.

As many market analysts point out, distressed homeowners frequently still have equity, which means foreclosure can often be avoided entirely.

That single factor dramatically reduces the chance of a foreclosure crisis.

📊 Why This Matters for the Housing Market

So what does all this mean?

Despite scary headlines, the data shows:

- Serious mortgage delinquencies are low

- Foreclosure filings are extremely low

- Homeowners have significant equity

- Lenders are working with borrowers to avoid foreclosure

Put it all together, and you get a market that’s far more stable than the one leading up to the 2008 crash.

Yes, the market is shifting.

Yes, some homeowners are feeling pressure.

But a mass foreclosure wave?

The numbers simply don’t support that narrative.

🏁 The Bottom Line

Foreclosures may be rising slightly—but context matters.

Compared to the housing crash, today’s numbers are dramatically lower, and homeowners are in a much stronger financial position thanks to rising equity and lending standards.

The takeaway?

Don’t panic over headlines. Look at the data.

And right now, the data says this market is built on a much stronger foundation than 2008.

Call or text us anytime at 855-935-MORE. We’d love to help.

Check out this article next