Don’t let confusing rates or bad data cost you your dream home! Download the Made 4 More app for the most accurate listings—without your info being sold—so you can compare homes, payments, and options with confidence. Get started today!

If you’ve been house hunting lately, you’ve felt it—affordability is tight. Payments are higher, rates are stubborn, and buyers are getting creative just to make the numbers work.

That’s exactly why Adjustable-Rate Mortgages (ARMs) are getting attention again.

But before you assume this is a hack to beat high rates, let’s slow down and talk about what an ARM really is—and whether it actually fits your plan.

🔍 What Is an Adjustable-Rate Mortgage, Really?

A fixed-rate mortgage is simple: your interest rate stays the same for the life of the loan. Predictable. Stable. Boring (in a good way).

An ARM? It starts with a lower fixed rate for a few years… and then it can change.

That means your payment could go up. Or down. Or up by a lot. It all depends on where rates are when the adjustment hits.

It’s the difference between locking in your payment long-term… and betting that future rates (and your finances) will work in your favor.

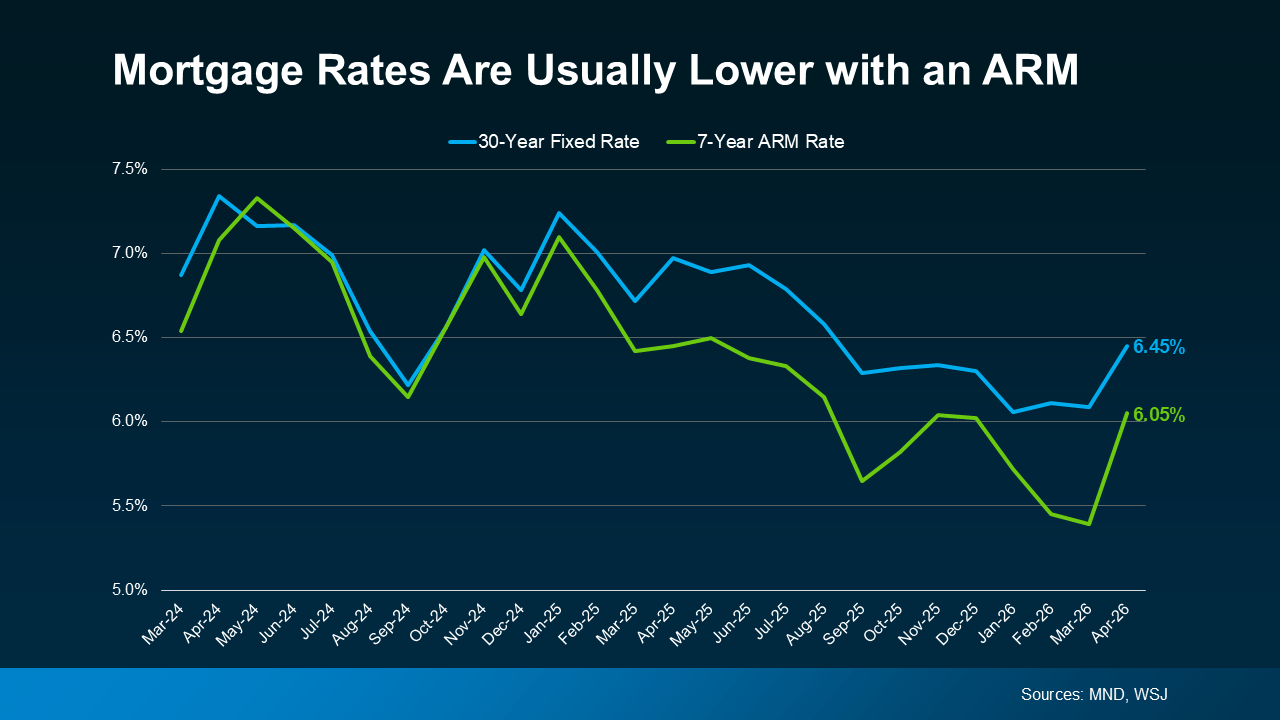

💸 Why Buyers Are Choosing ARMs Right Now

Here’s the part that gets people interested: the upfront savings.

ARM rates are typically lower than 30-year fixed rates. That lower rate can mean:

- A smaller monthly payment

- Or qualifying for a higher-priced home

- Or simply making the math work when it otherwise wouldn’t

For many buyers, that difference can be around $100–$200 per month. And in today’s market, that’s meaningful.

This isn’t about being risky. It’s about being strategic with affordability.

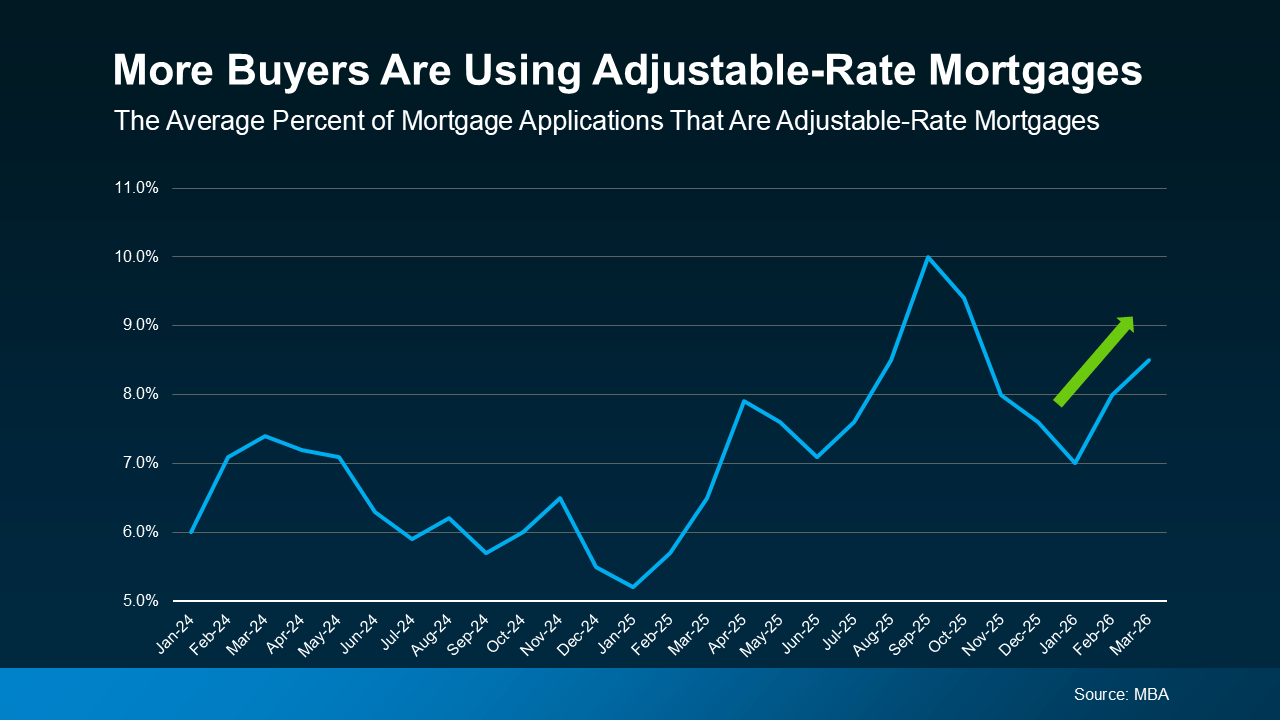

📈 Why ARMs Are Making a Comeback (Without the 2008 Vibes)

If you remember the housing crash, hearing ARMs are popular again might make you nervous.

But today’s ARMs are not the wild-west loans from back then.

Lenders now qualify buyers based on whether they could still afford the payment if the rate adjusts upward. Standards are tighter. Oversight is stricter. Buyers are more informed.

This isn’t a red flag for the market. It’s a sign buyers are adapting.

⚖️ The Trade-Off You Have To Think Through

Here’s the honest part.

An ARM can be smart if:

- You plan to move before the adjustment period

- You expect your income to increase

- You’re comfortable with some uncertainty later for savings now

But it can be stressful if:

- You plan to stay long-term

- Your budget is already tight

- You’re hoping rates will drop so you can refinance (no guarantees there)

An ARM is like taking the express lane now with the understanding the road may change later.

🧠 This Isn’t a Rate Decision. It’s a Life Plan Decision.

Choosing an ARM isn’t about chasing the lowest rate.

It’s about aligning your loan with your timeline, career path, risk tolerance, and long-term plan.

That’s why this decision should never be made without talking to a trusted lender who can map out real scenarios for you.

✅ Bottom Line

ARMs are helping buyers afford homes in the short term. But they’re not for everyone.

The key is understanding how they work, what could happen later, and whether that fits your strategy—not just your budget today.

📲 Call or text us at 855-935-MORE and we’ll connect you with a trusted lender to see if an ARM—or a fixed rate—makes more sense for you.

Check out this article next